Are Virtual Credit Cards Legal?

As businesses continue to embrace the remote work landscape, it is imperative to understand the options available to ensure employees have the tools they need to do their jobs, while also making sure processes are streamlined for your finance team, and sensitive information is not at risk.

Virtual credit cards are a great example of adapting to a new way of doing business—securely and conveniently. Virtual credit cards, or VCCs, were created to provide a way to mask secure information from being stolen. To do this, a one-time-use number is generated to hide sensitive credit card data when shopping online or with a mobile wallet. They are a great option for employers to issue to their workforce for one-time use, such as purchasing home office supplies online.

However, with new technologies and ways of doing business, questions often arise surrounding use cases and legality. VCCs are no exception. Let’s dive into how a virtual credit card is different from a physical card, if VCCs are legal, how they are regulated, and who this form of payment is best suited for.

Normal Credit Cards vs. Virtual Credit Cards

We’re all familiar with credit cards. It is a tangible form of payment issued for long-term use—normally three years after the card is first issued and activated. Traditional credit cards can be used online and in person with retailers. With magnetic strips being replaced by radio frequency identification (RFID) technology and chips, credit cards have become more secure over the years. However, its identifying information is still at risk of being stolen if a merchant is hacked.

A virtual credit card leverages electronic, cardless account numbers to allow for secure online payments. As we mentioned previously, “Virtual card numbers aren’t that different from a physical credit card.” Virtual cards include the typical 16 digit card number, an expiration date, and a security code, much like a regular credit card. Additionally, virtual credit cards offer an additional layer of security as the card number is linked to your account but does not reveal the real account number.

Further, virtual credit cards provide a faster and more secure alternative to issuing employees a physical corporate credit card to cover expenses.

Are Virtual Credit Cards Legal?

Major credit card companies like Mastercard, Visa, Capital One, and American Express issue virtual credit card numbers as a way to provide an additional layer of security for online purchases or to limit spend to an account. Virtual credit cards are completely legal and available for mainstream use.

In addition to virtual credit card numbers issued by the major card companies, there are also VCC generators. This option is legal to be used for card verification purposes that do not involve financial transactions, such as free trials. However, generated virtual credit card numbers that are not linked to an actual account can’t be used to pay for goods or services. These “fake” card numbers are useful for free trials where it is easy to forget to cancel a subscription to avoid fees.

Who Regulates Virtual Credit Cards?

While regulation specifically surrounding virtual credit cards is sparse, the credit card company issuing the virtual option has policies surrounding its use. For instance, Mastercard notes, “All debit payment products must adhere to the same regulatory standards, regardless of the type of business model which provides them or the manifestation of the product—physical card, virtual account number, cloud-based wallet, etc.”

Major credit cards issued by national banks are governed by the Treasury Department’s Office of the Comptroller of the Currency. As virtual cards continue to gain popularity and mainstream use, we anticipate additional regulatory oversight and governing parameters.

Who Should Get a Virtual Credit Card?

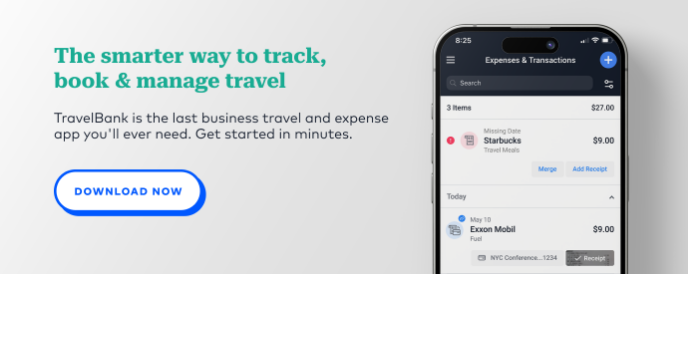

Virtual credit cards are a great option to keep information secure when shopping online or with a mobile wallet, especially for use by employees that may not require full-time access to a corporate credit card. Your finance team will know which employee makes a purchase as the number assigned will be unique and can set spend limits. Further, there will be no lag time while waiting for a physical card to arrive in the mail and the virtual card numbers are easy to activate and deactivate as needed. It will also make the reconciliation process at the end of the month easier as online purchases will be charged to the same account(s).

Conclusion

Virtual credit cards are 100% legal and accessible for both consumers and businesses. While VCCs can’t be used at stores without a mobile wallet, they are a great option for online purchasing that are more secure, prevent hackers from accessing identifying information, and easy to issue for individual employees as needed.

If you haven’t tested the virtual credit card waters and have more questions, please schedule a time to chat with our team. We have some additional tips and tricks you may find helpful.